A pretty good run! 4.01 miles in 1h 5min 55s, for an average pace of 16:25 and an average HR of 140 bpm. I don’t auto-pause the run tracking, so if I’m running a 14-minute mile (still pretty slow) and stop for 2 minutes to take a selfie for the blog, that shows as a 16-minute mile.

I just heard a teaser for a story on how PDFs have become ubiquitous, with the supposed downside that AIs have a lot of trouble reading a PDF. The implication was that was bad, but I thought “Awesome! I’m going to have to switch to PDFs for more of my output! Oh, and I think I’ll start using TeX to produce more of that output!”

If you’ve ever read the contents of a PDF file produced by TeX you’ll understand.

I’ve known since before the inauguration that the economy was facing stagflation. The tax cuts would boost the deficit, raising interest rates. The tariffs would boost prices, producing inflation. Both those things, plus forcing out immigrants, would tank the economy, producing stagnation (at best), yielding stagflation.

I wrote about this more than a year ago, in Our new upcoming stagflation. We are now seeing it, even before the war started.

I’m actually a little surprised we didn’t see it sooner. I credit the delay to a few things. First, Biden had left the economy in really good shape. It took a lot to tank it. Second, even though it seemed to us that Trump was “moving fast and braking things,” it’s just hard to move that fast on things like tax cuts, imposing tariffs, and deporting migrants—even if you’re willing to break laws to do it faster, these things take time. Third, Trump always chickens out, so we didn’t get the threatened tariffs on schedule; we got watered down tariffs after a delay.

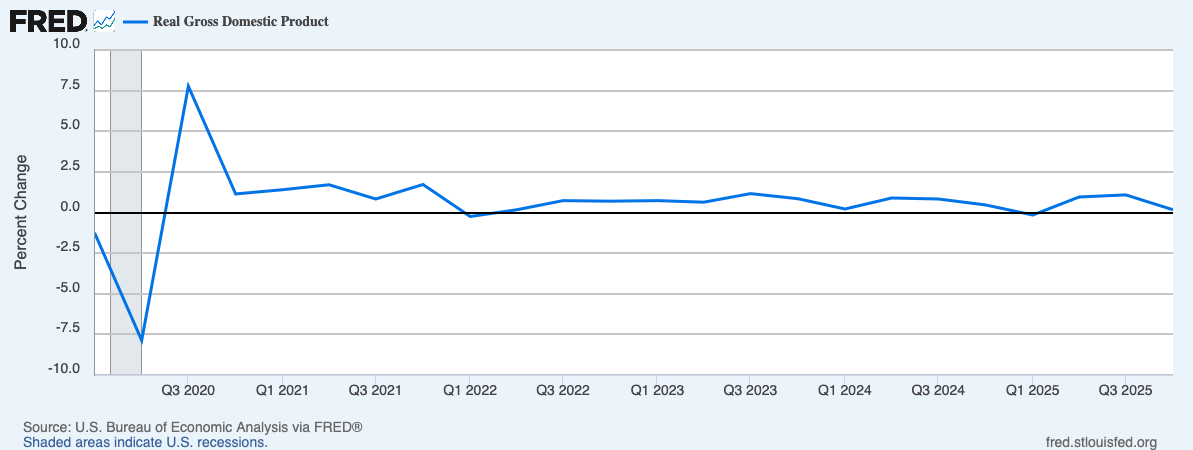

However, the stagflation is here. Check out this graph of Real GDP. As you can see, in Q4 it had fallen almost to zero. The economy wasn’t shrinking, but it was stagnating.

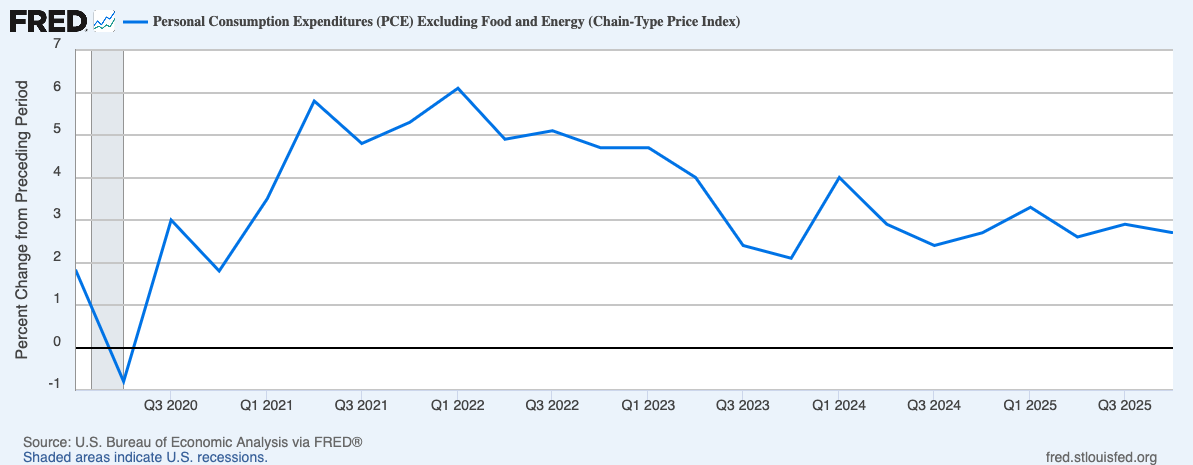

At the same time, inflation had quit coming down. Here’s a graph of Core PCE, the Fed’s preferred inflation index. After getting down almost to 2% (the Fed’s target) about 8 months ago, it reversed course and has been bumping along close to 3% since then.

I think all of these things were about to get worse. Even with the Supreme Court’s ruling that a major part of Trump’s tariffs were illegal, there were plenty of others that aren’t going away. The tax cuts are still in place. Immigration has virtually come to a halt, many immigrants have been detained or deported, and any sensible foreigners with skills that they can apply elsewhere are fleeing the country.

So: Stagflation was already here. But things are about to get much, much worse, because now there’s a war on.

That has already spiked up oil prices. Those won’t feed immediately into Core PCE (which excludes food and energy prices), but will feed in over time, because higher energy prices make everything we produce more expensive. And, of course, wars are fantastically expensive, meaning that the deficit will blow out way worse than it was already going to, which will lead to higher interest rates (soon) and higher taxes (later).

Oh, and don’t expect AI to save us. If you listen to the business news, you know that the only reason the economy isn’t in much worse shape is that businesses have been paying huge amounts on AI infrastructure. As I wrote in my AI bubble post, I think a large fraction of the data centers and model training that that money got paid for will turn out to be worth much less than was paid for it.

So, where are we? Well, about where I thought we’d be, as far as the economy goes—in a modest stagflation that could be fixed pretty quickly, at the cost of a substantial recession, if the Fed had the guts for that. Except that now we’re in a war too.

I can tell you how to arrange your finances to survive a stagflationary period, but I can’t tell you have to survive a war. Wars are very bad, much worse than recessions.

If you know how to survive a war, let me know. If not, good luck.

When I was 2 years old, I was in the hospital twice with digestive issues, and came out with a diagnosis of celiac.

This was in the very early 1960s, when nobody knew diddly squat about celiac, and there were no gluten-free baked goods, and no indications on labels or menus that all kinds of ordinary things in restaurants and grocery stores had gluten in some form or another. My mom did the best she could to avoid giving me things with gluten in them, and taught me to explain to people who were trying to feed me that I couldn’t eat wheat, oats, rye, or barley.

I think nowadays people think that oats don’t have gluten, but we didn’t know that then, so we did our best to avoid all of them.

I ate this half-assed gluten-free diet until 1976, when went away for 6 weeks to a National Science Foundation summer program. I was living in a college dorm and eating in a college cafeteria, and found it too difficult to follow my diet. I found that my digestion was about the same as before, and just quit worrying about staying gluten-free. (Until I got married, and my wife thought that, if I had celiac, perhaps I should avoid gluten. And it was much easier in the 1990s to find gluten-free food.)

Fast-forward another decade or so. Blood tests for the antibodies to gluten became available. I got those tests done, and discovered that I’d never had celiac.

So, one thing I like to do these days is hark back to having to avoid “wheat, oats, rye, or barley,” and subvert it, by baking bread that contains wheat, oats, rye and barley.

In the years that I was particularly suffering from season depression in the winter months, I found various things that helped. (Click the SAD tag to see various posts on the topic.) One thing that was kind of in the middle in terms of both value and effort was taking myself on an Artist Date. (There’s an Artist Date tag as well.)

Lots of different things can quality as an Artist Date, of course, but I usually used the term to refer to going to someplace (anyplace) that I found inspired me. At the top of the list, because there’s already art, which helps me get into the right frame of mind, is to go to an art museum or an art gallery. But almost as high is going to a natural area, or some place like the Japanese Garden at Japan House.

I haven’t been particularly depressed this winter, but the Krannert Art Museum had an exhibit of textile art that Jackie wanted to see, so we decided to make an artist date of it. On a whim, we added the Conservatory, which has a greenhouse with a bunch of tropical flowers, and is always nice to visit in the winter, because it’s warm and sunny. (Sunniness, of course, depends on the sun being out.)

It’s hard to get a good picture of the art museum, except by just taking pictures of individual works of art, which I don’t like to do (out of courtesy and for copyright reasons), but I thought this one was valid:

There was a term (that I have already forgotten) for having numerous paintings covering the wall, rather than a spaced array of individual paintings.

And this one was produced as part of the WPA’s Federal Arts Project, by artists who were paid a modest wage to make art that belonged to the government (and all such work is copyright-free):

As I said, I wasn’t really depressed, so it didn’t so much matter that the Conservatory greenhouse gave of a clear view of the complete lack of sun:

For the first couple of years I was doing longsword, I had real trouble keeping my arms extended and pushing my hands up (due to a lack of strength, lack of endurance, and lack of the habit).

I did all manner of training to work on this—exercises for arm strength, especially overhead pushing, endurance training for those same exercises, and of course sparring to train the habit. (See in particular Fitness training for longsword.)

I’m not there yet, but it no longer seems to be my worst problem. Here’s a sparring match with one of the better fencers in our local group:

I’m not quite all the way there, so it’s a thing to keep paying attention to, but it’s no longer my biggest problem.

A pretty good recent episode of Gil Duran’s Nerd Reich podcast had an odd hole in it.

In the one I’m talking about, the one with Quinn Slobodian, Quinn explains that there’s a reason the many efforts to create a seastead, charter city, network state, and such never go anywhere: They’re unnecessary.

[Y]ou don’t actually need to create a new polity to have your own sense of entitlement and privilege reinforced in every imaginable way, and to have your own economic comfort facilitated by the institutional arrangements of the state in almost every way. With some creative accounting and some use of offshore havens and trusts and so on, you can really game the whole thing very well already, right?

Having said that, they do talk a bit about why, given that there are already tools to protect your property and money (freeports, trust, special economic zones, and the like), anybody would work so hard and spend so much money to create an actual place that’s outside the control of any government. They don’t quite come around to answering that question, which I think is unfortunate, because I think they both know the answer.

The people pushing these efforts want serfs.

They don’t want workers who can join unions. They don’t want software engineers who hesitate to create autonomous munitions or tools for surveillance capitalism. They don’t want maids or pool boys who feel free to resist their advances.

They want the right to be mean to people, in a situation where the people have to just take it.

That’s what places like Próspera offer that you can’t get from a family company incorporated in a special economic zone.

Stephen Miller would have ICE agents (and the rest of us) believe that they have “immunity” to perform their “duties.”

This is, of course, false. Depriving any person (not just citizens) of their rights “under color of law” is its own crime. But it is in that light that we should view their position on face masks as admitting that they know they have it wrong:

The administration’s perceived need for face coverings evocative of Iranian secret police and Russian security agents helps us recognize that assertions of state supremacy and citizen insignificance are claptrap…

If they were immune, they’d not hesitate to show their faces. The fact that they feel the need to keep them hidden makes it very clear that they know they’re totally exposed in a legal sense.

Ten years ago, instead of taking Jackie out to a restaurant and sitting with a bunch of other couples wanting to overpay to order off a “special” Valentine’s Day menu, I decided it would be more fun to cook her my own little feast.

As my inspiration, I reached back to October, 1991, and the very first meal I ever cooked for her. (She was threatening to go home because she was tired, and I said, “No! Stay here! I’ll fix dinner! You can just take a nap and I’ll do everything!”)

Some of the details have varied (the flourless chocolate cake was new maybe 4 years ago), but rock cornish game hens and long-grain and wild rice have always been there.

Okay, this is really, really good. About writers and writing (via @doctorow).

Makes me want to write some proletarian literature.

Characters in proletarian literature are often misled into believing that their individual flaws account for their miserable conditions, but then encounter a union organizer or a wise old Wobbly who tells them the truth, setting fictional men and women on the revolutionary path.

Three or four years ago I got a pair of LL Bean Cresta pants, which proved to be very satisfactory hiking pants: Fit me, okay in rain or wind, sturdy enough, excellent pockets for hiking.

(They turned out not to be sturdy enough to stand up to the depredations of a puppy, but that’s neither here nor there.)

That winter I bought a pair of Crest lined pants, which turned out to be similarly excellent: All the things I liked about their summer pants, plus nicely warm, without being so bulky or so insulated as to be a problem.

I’ve had them for a couple of winters now, but until this year, I didn’t actually wear them much. It’s quite typical to have two or three or four really cold days in a winter, maybe even two periods like that. But really, one pair of lined pants nicely does the trick. I wear them for my dog walks until the cold breaks. Then I wash them, and they’re available for the next cold snap.

This year has been different. Cold, cold, and more cold. More than a week ago I looked at the forecast, and realized that I’d be better off with a second pair of these pants.

So, I ordered a second pair. They came yesterday. So last night I put my previous pair in the laundry and today I wore my new pants for my first two dog walks.

Once again, most satisfactory.

(It’s too hard to take a selfie that includes my pants, so instead here’s a picture of Ashley. I wanted to give her neck a good scritching, so I took her collar off, so she’s all naked.)

This is exactly right, and we’re all going to suffer for it (along with all the other things we’re going to suffer for because of Trump).

The best summary of Trump’s trade “philosophy” comes from Trashfuture’s November Kelly, who said that Trump is flipping over the table in a poker game that’s rigged in his favor because he resents having to pretend to play the game at all.

There’s a broker offering a new product, that I’d have been all over 30 years ago. I think they’re calling it a “generated asset,” where they create a personal stock index just for you (based on a prompt to an AI), and then create an imaginary index fund for that imaginary index, and then (I assume) invest in the underlying stocks on your behalf.

Of course, you could do that yourself, but it would be awkward, probably expensive, and definitely fiddly, with a need to track the index over time.

So, instead of that (I assume), the company just promises to pay you the value of your index, and (I assume) hedges its promise by holding the underlying shares—and since this synthetic investment is a service, they can lump all these promises together and invest in all the underlying shares, and be generally sure that their hedge will be close enough that even very large stock moves won’t cost them more than investors are paying for access to this service.

As I said, I’d have been all over that 30 years ago. Now, not so much. I’ve gotten lazier and more conservative with my investments as I’ve gotten older.

But it did make me think what I’d want to invest in, if I were to create a synthetic index, and it occurred to me that the companies that are putting the least amount of money into AI crap will do much better over the next few years. So I asked confer.to if it could give me “a list of large corporations ordered by how much they talk about AI in their reports to investors.”

Sadly, the answer was no:

Based on the available data, I can’t provide a specific ranked list of large corporations ordered by how much they discuss AI in their earnings reports. While the information confirms that AI is a major topic in 2025 earnings calls across the S&P 500, the detailed company-by-company ranking you’re looking for isn’t publicly available in the sources I checked.

Here’s what we do know:

AI is a dominant topic: In Q3 2025, “AI” was cited on 306 S&P 500 earnings calls, the highest number in the past decade.

Significant increase: This is a large jump from the five-year average of 136 mentions and the 10-year average of 86.

Sector leaders: The Information Technology (95%) and Communication Services (95%) sectors have the highest percentage of companies mentioning AI.

Market impact: Companies that mentioned AI in their Q3 2025 calls saw a higher average stock price increase (13.9%) compared to those that didn’t (5.7%) since the end of 2024.

While sources like Yahoo Finance and MacroMicro track the overall trend and volume of AI mentions, they don’t publish a specific, ordered list of corporations ranked by the frequency or depth of their AI discussions in earnings reports.

This type of granular, ranked data is typically compiled by specialized financial data and analytics firms (like FactSet, which provided the data to Yahoo Finance) and is often part of a paid subscription service.

Perhaps the specialized AI tool that this broker uses to create its imaginary indices has access to the fine-grained data about AI mentions in earnings calls with investors. But I don’t care enough to go to the trouble of looking.

Poking around at the St. Louis Fed’s Fred graphing tool (to come up with a graphic to include for this post), though, led me to the graph at the top, which is of the “Nasdaq Global Artificial Intelligence and Big Data Index,” which “is designed to track the performance of companies engaged in the following themes: Deep Learning, NLP, Image Recognition, Speech Recognition & Chatbots, Cloud Computing, Cybersecurity and Big Data.”

So one option to get what I want would be to just go short on that index.

Turns out Cory Doctorow and I think a lot alike about the AI bubble, but he also has stuff to say about how to speed along the popping of the bubble, which would be a good thing. (Bubbles that pop sooner do less damage when they do.)

so I’m going to explain what I think about AI and how to be a good AI critic. By which I mean: “How to be a critic whose criticism inflicts maximum damage on the parts of AI that are doing the most harm.”

My father was great. This post isn’t really about all that, though. It’s about one (or two) specific things my dad did that have proven to be very beneficial to me.

One was that my dad was big on looking at things. I assume this mostly came from his being an ornithologist, which to a great extent involves looking at little tiny things some distance away.

He was always encouraging me to look for and look at things in the distance. On long car trips he’d often encourage me to watch for things like the water towers with the names of each town we were approaching. I’m sure part of that was just to keep me occupied with something other than complaining about being in the car, but part of it was getting me good at watching for things coming over the horizon, a skill that has proven itself of great value, even though I’m not a fighter pilot, or a lookout in a ship’s crows nest.

The other thing, closely related, was my father’s enthusiasm for praising specific things, of which this was one. Anytime I’d spot something early—especially if it was earlier than he did—he’d say, “Good eye!” He did that a lot when I was a boy, but he never really stopped. I remember just a few years before he died, I spotted a Hooded Warbler outside the house where he was living in Kalamazoo and drew a “Good eye!”

Even though I don’t have kids, I try to do this with other folks around me. A little praise never hurt anyone, and being able to spot things in the distance is always useful.

See the horse in the picture at the top? Maybe this will help a little:

Back in May, I wrote an article about AI journaling. The idea (which I had stolen from some YouTuber) was that you write your journal entries as a brain dump—just lists of stuff—into an LLM, and then ask the LLM to do it’s thing.

. . . ask the LLM to organize those lists: Give me a list of things to do today. Give me a list of blind spots I haven’t been thinking of. Suggest a plan of action for addressing my issues. Tell me if there’s any easy way to solve multiple problems with a single action.

Now, I think it’s very unlikely that an LLM is going to come up with anything genuinely insightful in response to these prompts. But here’s the thing: Your journal isn’t going to either. The value of journaling is that you’re regularly thinking about this stuff, and you’re giving yourself a chance to deal with your stresses in a compartmented way that makes them less likely to spill over into areas of your life where they’re more likely to be harmful.

I still think that’s all true, and I still think an LLM might be a useful journaling tool. My main concern had to do with privacy. I didn’t want to provide some corporation’s LLM with all my hopes, dreams, fears, and best ideas, and hope that none of that data would be misused. I mean, bad enough if it was just subsumed into the LLMs innards and used as a tiny bit of new training data. Much worse if it was used to profile me, so that the AI firm could use my ramblings about my cares as an entry way into selling me crap. (And you know that selling you crap is going to be phase two of LLM deployment. Phase three is going to be convincing you to advocate and vote for the AI firm’s preferred political positions.)

Anyway, I figured it wouldn’t be long before local LLMs (where I’d actually be in control of where the data went) would be good enough to do this stuff, and I was willing to wait.

But I didn’t even have to wait that long! A couple of days ago, I saw an article in Ars Technica describing how Moxie Marlinspike of Signal fame had jumped out ahead with a really practical tool: confer.to. It’s a privacy-first AI tool built so that your conversation with the LLM is end-to-end encrypted in a way that keeps your conversation genuinely private.

I’ve started using it for journaling exactly as I described. Because of the way the privacy is inherent to Confer, I can’t actually keep my journal within Confer—all the content is lost when I end the session. So, I’m keeping the journal entries in Obsidian, and then copying each entry into Confer when I’m ready to get its take on what I’ve written.

I wanted some sort of graphic for the post, and asked Confer to suggest something. It came up with 5 ideas, including this one, which (bonus) actually illustrates my process:

Anyway, I’ve already written three journal entries that I otherwise wouldn’t have, and gotten some mildly entertaining commentary on them—some of which may rise to the level of useful. We’ll see.

(Asked to comment on a previous draft of this post, Confer.to mentioned the “Give me a list of blind spots I haven’t been thinking of,” prompt above, and said, “But LLMs can’t actually know your blind spots — they can only reflect patterns in what you’ve said.” Which I know. And so, of course, once I started using an actual AI tool instead of just an imagined one, that ended up not being something I asked for.)

If I keep doing this (and I think I will), I’ll follow up with more stories from the AI-enhanced journaling trenches.

Next weekend is going to be pretty cold in Minneapolis. Maybe cold enough to convince some ICE goons that they’d be better off on disability in Kentucky.

I mean, every ICE goon has probably slipped on the ice at least once. Probably every one of those falls could be turned into a disability claim.

I am (just barely) old enough to remember the Black Panthers in the 1960s, when a group of black people tried to carry legal firearms to protect themselves, before they were mostly murdered by the police, the FBI, and one another.

I also remember the 1980s, when the NRA was trying to convince all marginalized groups (blacks, women, lesbians, gays, socialists, etc.), that arming themselves was a great idea. The NRA was sincere, I think—they just wanted more people to have guns.

Most people, especially black people, were well aware of the fact that walking around armed would make it much more likely that they’d be killed by the police. (They remembered what happened to the Black Panthers, presumably better than I did.)

Over the last couple of years, and especially over the last few days, I think perspectives are changing. First, a lot of white people are walking around armed, and even killing people, with minimal consequences. Second, the increasingly fascist police have been killing unarmed people at increasing rates, and looking like they’ll not only get away with it, but looking like they’re glorying in it.

This article, which had a really annoying headline, turns out to have some really great thinking.

In particular, the political perspective it is describing has more than a little overlap with the stuff I was writing about in my articles at Wise Bread.

An economic vision that … encompasses antimonopoly policies, right to repair and regulatory changes to smooth the path for people to start businesses, buy and work land, even build their own houses and invent things.

Steven suggested that I should revisit my Wise Bread posts. There’s a lot of useful stuff there. It was stuff that had seemed a bit less relevant over the last few years (I started writing in June of 2007, right at the start of the Great Financial Crisis, and carried on for 10 years.) But with government having gone all-in on fascism, racism, and gangsterism this year, a lot of those themes are feeling much more on point than they had for a while.

So I think I’ll do that. A lot of my Wise Bread posts still feel just right. On a few, my perspective has changed a bit. I’ll write some new posts to talk about what’s changed.